The TV industry is at a pivotal moment, facing the same kinds of digital shifts that rocked the music world over the past two decades. Just as MP3s transformed how we listened to music, streaming platforms like Netflix, Hulu, and Amazon Prime Video are reshaping how we consume video content. But the music industry didn’t adapt without challenges – formats evolved, piracy surged, and record labels had to rethink distribution.

To understand where TV might be heading and how advertisers can leverage these shifts, we can look at music’s evolution and consider how its journey from physical formats to digital streaming inform the future of TV.

The Shift to Digital: TV’s Parallel with Music and Its Hurdles

TV has often followed music’s lead in adopting new formats and technologies. Just as radio gave rise to TV, physical formats like CDs transitioned to DVDs, and MP3 players paved the way for iPods and smartphones. While music had an advantage in going digital with audio being easier to compress to new formats than video, TV is now in its own era of on-demand, digital distribution thanks to advances in technology.

This parallel is no coincidence; the major music labels – Universal Music Group, Warner Music Group, and Sony Music – are closely tied to entertainment studios, such as Sony Music’s connection to Sony Pictures. These intertwined industries face similar challenges and opportunities in the digital space.

However, TV’s shift to digital is slower due to unique challenges. While the music industry quickly adapted to digital formats to meet shifting consumer demand and combat piracy, TV content is often restricted by long-term licensing agreements and high production costs. Unlike music, where a few major players control vast catalogs, TV content is also fragmented across many rights holders.

Moreover, TV relies on cyclical media rights agreements, often on 5 to 10-year cycles for premium content. For example, the NFL’s media rights will be up for renewal in five years, and the NBA’s recent contract negotiations will be renewed again in eleven years. Throughout these cycles, studios and streaming platforms are under financial pressure to prove the value of the programming content with changing viewership behaviors.

Tackling Piracy: How Music’s Digital Transformation Holds Clues for TV

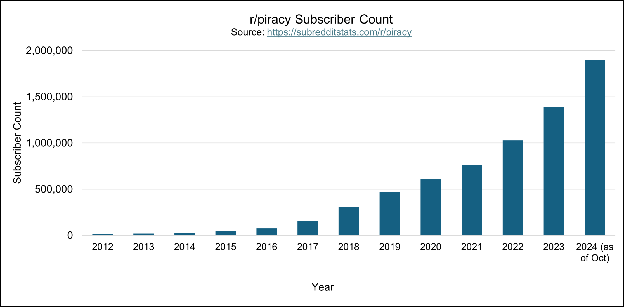

Just as the music industry struggled with a rise in piracy in the 2000’s, the TV and Film industry are now facing similar growing challenges. As more and more streaming services have launched, content has become more scattered and costly, driving a growth towards piracy. For instance, Reddit’s subreddit r/piracy has grown to 1.9 million subscribers as new services like ESPN+ (launched in April 2018), Peacock (April 2020), and Paramount+ (March 2021) entered the market. Recent news from June 2024 also highlighted an illegal streaming service which boasted a larger catalog of content than Netflix, Hulu, and Amazon combined at just $9.99 per month (source: Variety).

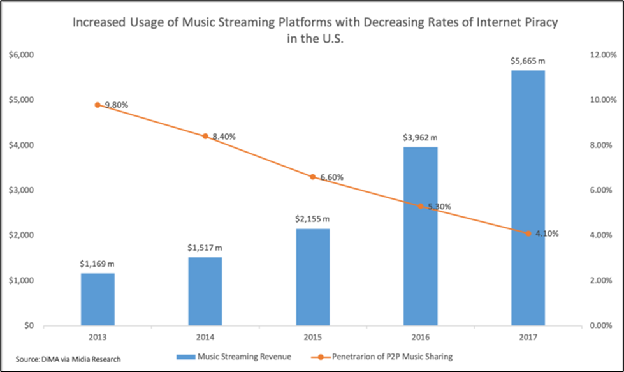

While the music industry initially fought piracy with litigation, the major record labels ultimately embraced digital platforms to offer affordable, legal options that gave consumers easy access to music. As music streaming services became more accessible, piracy declined and revenues for the music industry surged, growing from $10.5 billion in 2017 to $17.1 billion in 2023 (RIAA).

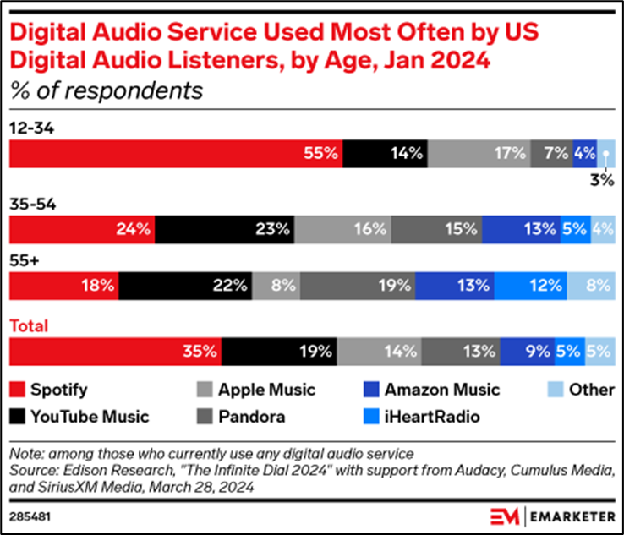

Today, subscription and ad-supported music streaming now account for over 70% of the music industry’s total revenue, with just a handful of major players like Spotify, YouTube Music, and Apple Music driving most of the usage (68%) for the digital audio market.

The State of Streaming TV: Revisiting the Cable Model

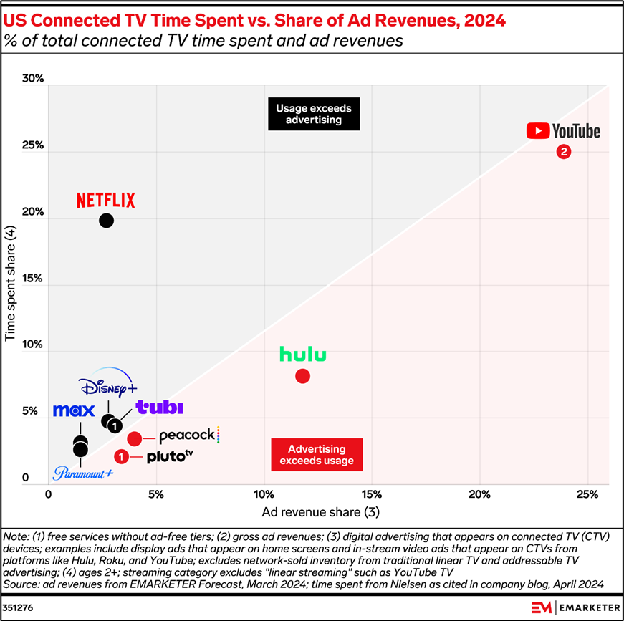

Interestingly, streaming TV has started to resemble the traditional cable business model. Many platforms now offer ad-supported tiers and bundle services, helping streaming turn a profit by revisiting the cable playbook, as The Drum recently overviewed (The Drum). However, ad spending is spread thin across platforms with few capturing more than 5% of ad revenue share, posing a challenge in trying to maximize reach.

Subscriber churn is also rising as streaming costs increase. A Deloitte study shows that 64% of consumers are frustrated with subscription costs, and 44% have canceled at least one subscription recently (MediaPlay News).

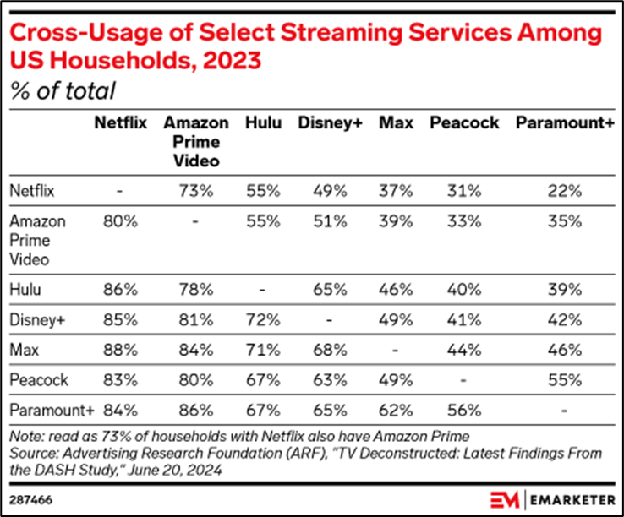

To combat churn, platforms are increasingly looking towards bundling, and newer entrants like Paramount+, Peacock, and Max are positioned well for bundle deals to attract a broader audience due to lower cross-usage with other platforms.

Additionally, streaming services have increasingly been forming strategic partnerships to boost consumer engagement and potential reach, similar to how the major record labels ultimately partnered with social platforms to allow the use of their music for promotional use. For example, Peacock, Disney+, Max, and Paramount+ recently joined forces with grocery delivery apps (Hollywood Reporter) while Apple TV+ is teaming up with TikTok to promote MLS (Marketing Brew).

Preparing for the Future: Further Consolidation in Streaming TV

Over the next 5–10 years, consolidation will likely continue to reshape the streaming TV landscape as high operational costs and the next cycle of media rights negotiations put pressure on platforms. The streaming platforms best positioned to thrive are those with deep financial resources and established digital infrastructures with broad reach, such as Netflix, Amazon, YouTube/Google, or Hulu/Disney+. Other platforms may be required to pivot or merge to remain competitive.

Sony Pictures, for instance, was one of the first players in streaming when it bought Crackle in 2006 and launched their vMVPD platform, PlayStation Vue, in 2015. However, due to the high costs of maintaining these direct-to-consumer services, Sony ultimately shifted to a content licensing model and become more of an “arms dealer” in streaming. The recent bankruptcy news of Chicken Soup for the Soul, the current owner of Crackle, further highlights the financial challenges in operating independent streaming services (NPR).

Meanwhile, consumers increasingly prefer a unified streaming experience. Parks Associates reports that over half of connected TV households favor a single ecosystem for easier app management (TV Tech). This trend hints at the potential for an integrated streaming hub that offers diverse content in one place – Amazon’s Prime Video Channels, which offers additional subscriptions like Paramount+ and more recently Apple TV+, demonstrates this point (New York Post). As noted in the NY Times article “The Future of Streaming (According to the Moguls Figuring It Out)”, industry vets are also predicting further bundling and consolidation that will lead to what Jason Kilar, former chief executives at Hulu and WarnerMedia, referred to as a “Spotify for Hollywood”, where studios would contribute to a singular platform to enhance the consumer experience (NY Times).

Takeaway for Advertisers

Music’s journey to digital underscores the importance of adaptability. For TV advertisers, the future is full of opportunities, but success depends on readiness to pivot. Embracing ad-supported models, bundling, and strategic partnerships will be crucial for streaming platforms in capturing today’s fragmented audiences

While we may see increased consolidation over the coming years, advertisers should understand the current landscape to excel in today’s hybrid environment. Partnering with experts who can navigate both traditional TV and streaming will provide brands with a strong advantage in staying ahead.

Let’s connect to discuss the future of TV and how Three First Names & Associates can help you succeed in the CTV space!