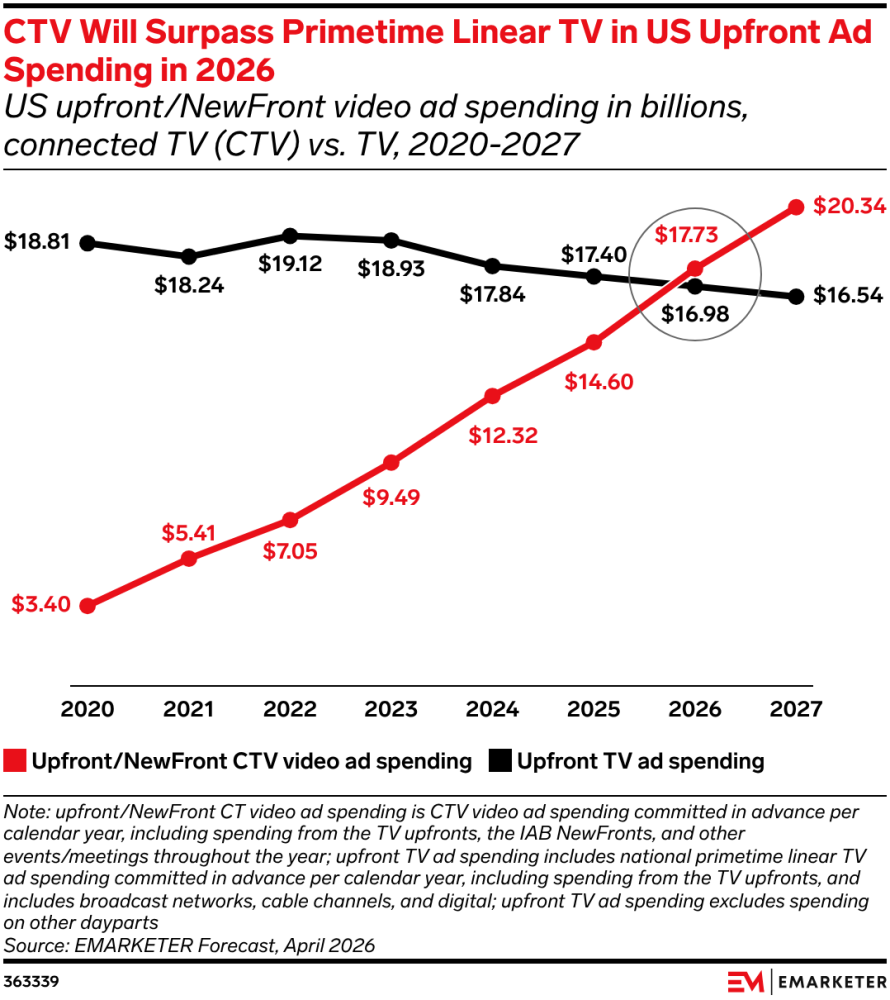

There is always a lot of noise around the TV Upfronts each year.

Between the press coverage, presentations, and the $30B+ in ad spending expected to be transacted across the Upfronts and NewFronts in 2026, the conversation often centers on whether the Upfront model is still relevant as streaming and programmatic continue to grow.

However, that framing misses how the market actually operates today. Traditional TV buying and programmatic are often positioned as competing approaches when in practice they are part of the same system.

Background on TV Upfronts

For those less familiar, the TV Upfronts are a buying period in late spring where major media companies sell advertising inventory for the upcoming broadcast year in advance.

The model dates back to the early days of broadcast television, when audience measurement relied on Nielsen “sweeps” periods and manual tracking methods. Upfront commitments created efficiency for both buyers and sellers by allowing large portions of inventory to be transacted ahead of time rather than through individual deals.

That structure has remained, but the way advertisers engage with it has evolved.

Over the past decade, several shifts have changed how the Upfront is approached:

- Increased demand for flexibility in commitments

- The rise of alternative measurement providers beyond Nielsen

- Greater access to performance data for advertisers

- A shift away from “set it and forget it” planning toward more continuous optimization

As a result, the Upfront now operates as one component within a broader allocation strategy rather than a standalone approach.

At the same time, its role remains meaningful.

A small number of media companies control the majority of TV viewership, making relationships with these partners critical for accessing premium inventory and achieving scale.

This is also reflected in how streaming platforms are evolving:

- Netflix introducing multi-year deal structures (source)

- YouTube incorporating traditional TV staples like makegoods (source)

- Broader industry recognition that linear TV and streaming are complementary (source)

Taken together, these changes point to a market that is converging rather than replacing one model with another.

To make this more practical, it helps to break down the different ways TV is bought today across both traditional and programmatic as well as how those approaches connect to each other.

Traditional TV Buying

Upfronts

What it is: Annual commitments made in advance to secure inventory, pricing, and audience delivery.

Benefits & Purpose

- Guaranteed access to premium inventory and key programming

- More predictable pricing and delivery

- Stronger relationships with media partners

- Ability to secure high-demand cultural moments

Drawbacks & Considerations

- Reduced flexibility to shift budgets mid-flight

- Risk of overcommitting if performance is not closely managed

- Requires confidence in long-term strategy

Scatter

What it is: Inventory purchased closer to air date, outside of Upfront commitments.

Benefits & Purpose

- Greater flexibility in budget allocation

- Ability to react to performance and market conditions

- Access to opportunistic inventory

Drawbacks & Considerations

- Pricing volatility

- Limited guarantees

- Less consistent access to premium inventory

Direct Response / Remnant

What it is: Lower-cost inventory focused on driving immediate performance outcomes, typically purchased closer to air time.

Benefits & Purpose

- Cost efficiency

- Useful for testing and validating TV as a channel

- Strong alignment with performance-driven objectives

Drawbacks & Considerations

- Limited scale and reach

- Lower-quality inventory environments

- Less effective for brand building

Programmatic CTV Buying

Direct / IO

What it is: Direct deals between buyer and publisher, often executed through traditional insertion orders.

Benefits & Purpose

- Closer proximity to supply

- Greater transparency and access to data signals

- Stronger control over placement and environment

Drawbacks & Considerations

- Less scalable than programmatic activation

- More manual execution

Programmatic Guaranteed (PG)

What it is: Automated direct deals that guarantee inventory and pricing between buyer and seller.

Benefits & Purpose

- Combines guaranteed access with programmatic execution

- Streamlined workflows through DSPs

- Maintains predictability while enabling targeting

Drawbacks & Considerations

- Still requires upfront commitment

- Less flexible than auction-based buying

Private Marketplaces (PMPs)

What it is: Invitation-only auctions where select buyers can access premium inventory.

Benefits & Purpose

- Greater control compared to open exchange

- Access to higher-quality inventory

- Ability to layer in audience and contextual targeting

Drawbacks & Considerations

- No guaranteed delivery

- Pricing can increase in competitive environments

Open Exchange

What it is: Real-time, auction-based buying across a broad pool of inventory.

Benefits & Purpose

- Maximum flexibility

- Scalable reach

- Efficient for performance-driven campaigns

Drawbacks & Considerations

- Variable inventory quality

- Limited transparency into underlying signals

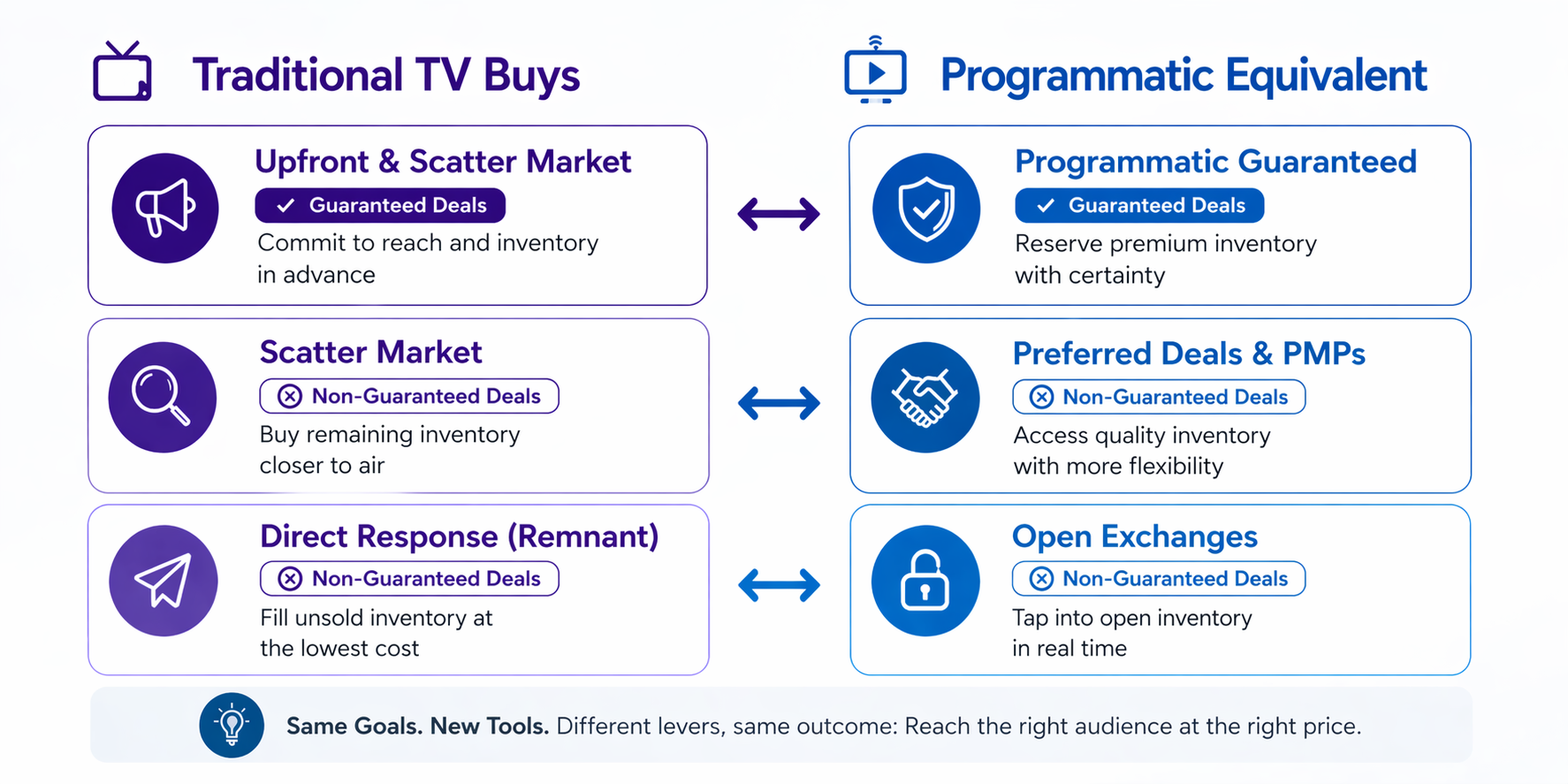

How Traditional TV and Programmatic Buying Compare

At a high level, the mapping is straightforward:

- Upfront → Programmatic Guaranteed

- Scatter → PMPs / Preferred Deals

- DR/Remnant → Open Exchange

The structure is consistent across both environments even as execution has evolved.

Since a brand’s media buy is an investment, a helpful way to translate these dynamics is through a financial lens.

Financial Portfolio Comparison

Upfronts / Scatter = Futures Market

- Commitments are made in advance to secure pricing and access to inventory that may become more expensive or unavailable later.

Programmatic = Stock Market

- Inventory is purchased dynamically in real time with pricing fluctuating based on demand and availability.

AI Models / Curation = Index Funds

- Optimization models allocate spend across inventory sources based on performance signals.

The most effective strategies tend to reflect a balanced portfolio rather than relying on a single approach.

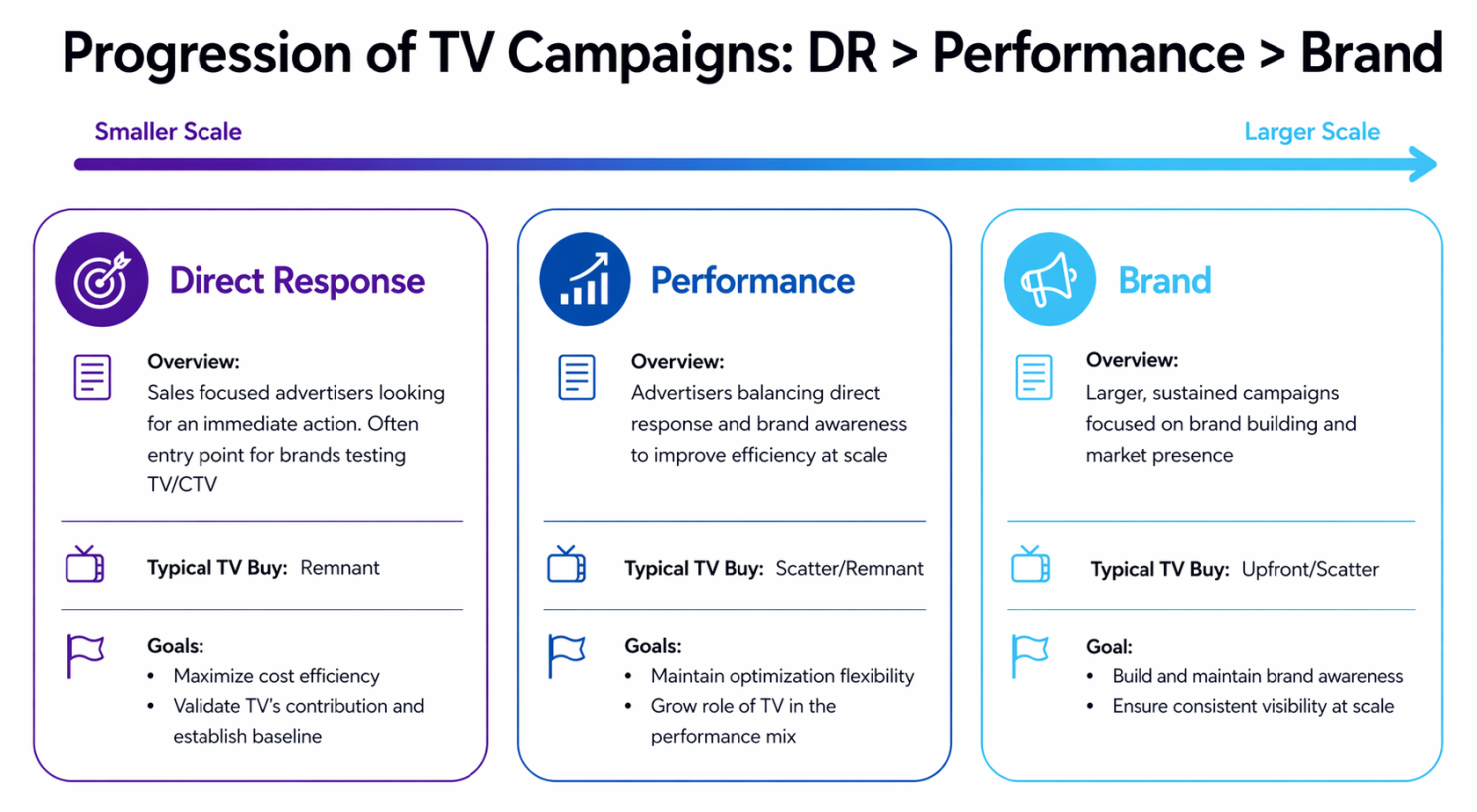

Are the Upfronts Worth Considering?

The answer depends on an advertiser’s size, objectives, and stage of growth.

- Emerging / DTC brands: Often lean toward programmatic and remnant inventory to prioritize efficiency and testing

- Performance / Growth brands: Balance flexibility with selective guaranteed investments

- Established brands: Rely more heavily on Upfront and Programmatic Guaranteed to secure scale and consistency

A common challenge across these groups is shifting strategies too frequently.

In many cases, the issue is less about access to data and more about how the buy is being approached – TV still requires consistency to build reach and allow performance to compound over time, similar to how TV shows can take multiple seasons to build a loyal audience following.

A Real-World Example of the Shift

In working with a large, digitally native advertiser, one of the biggest challenges was reframing how they approached Upfronts.

The initial instinct was to reduce long-term commitments and rely more heavily on programmatic to maintain flexibility.

Over time, the approach shifted toward:

- Maintaining partnerships with key media companies

- Securing access to high-impact inventory

- Using programmatic and scatter to optimize around that foundation

This led to more consistent reach across campaigns along with improved efficiency from optimizing incremental spend.

The shift was less about replacing one approach and more about building a more balanced allocation.

Conclusion

Programmatic advertising is already complicated enough for most organizations. Adding in decades of somewhat antiquated traditional TV buying practices can make the landscape feel even more fragmented, particularly for brands newer to the channel.

It becomes easier to figure out once the relationships between these approaches are clear.

- Traditional TV and programmatic are converging

- Fixed commitments are being supplemented with more flexible allocation

- Planning is shifting toward continuous optimization

- Measurement remains fragmented across linear and streaming environments

The advertisers that navigate this effectively tend to focus less on choosing between approaches and more on how they fit together within a broader strategy.

At a foundational level, the buying approaches themselves remain familiar even as the tools and execution continue to evolve.

Final Thoughts

For brands navigating these dynamics, the challenge is rarely access to inventory or data. It is understanding how to connect the pieces in a way that aligns with business objectives and scales over time.

If you’re working through similar questions around TV/CTV and programmatic strategy, feel free to reach out or connect with Nathan Scott at Three First Names & Associates!

At Three First Names & Associates, we bring a unique and forward-thinking approach to Connected TV by combining a deep expertise in TV advertising with a creative passion for the music industry. Founded by Nathan Michael Scott, our consulting firm leverages nearly a decade of experience in media and advertising to guide brands and agencies through the transition from traditional TV to streaming.